Getting a loan with bad or no credit can feel impossible and lots of people worry they will never get approved. But over 16 percent of Americans have credit scores below 580, which is officially considered poor. What surprises most is that lenders are now using more than just credit scores to make decisions, and solid proof of income or a bigger down payment can tip the odds in your favor.

Table of Contents

- Understanding Approval Requirements For Bad Credit

- Key Steps To Boost Your Approval Chances

- Special Strategies For First-Time Buyers And Self-Employed

- Common Mistakes That Cause Declines

Quick Summary

| Takeaway | Explanation |

|---|---|

| Understand Credit Score Categories | Credit scores range from poor (300-579) to good (670-739), impacting loan approval terms and requirements. Familiarity with these categories helps set realistic expectations for applicants. |

| Prepare Comprehensive Documentation | Gather key documents like pay stubs, tax returns, and bank statements to demonstrate financial stability and reliability, enhancing your approval chances. |

| Avoid Common Mistakes in Applications | Review and correct any credit report inaccuracies, maintain low debt-to-income ratios, and provide consistent information to prevent automatic declines from lenders. |

| Utilize Alternative Financing Methods | Explore lenders who focus on holistic evaluations beyond traditional credit scores, especially if you have bad or limited credit history, to improve your approval opportunities. |

| Consider Larger Down Payments | Offering a larger down payment reduces lender risk and may increase your chances of securing financing, showcasing financial commitment and planning. |

Understanding Approval Requirements for Bad Credit

Navigating auto financing with bad or no credit requires understanding the complex landscape of approval requirements. Lenders evaluate multiple factors beyond traditional credit scores to determine an applicant’s eligibility and risk profile.

Credit Score Categories and Their Impact

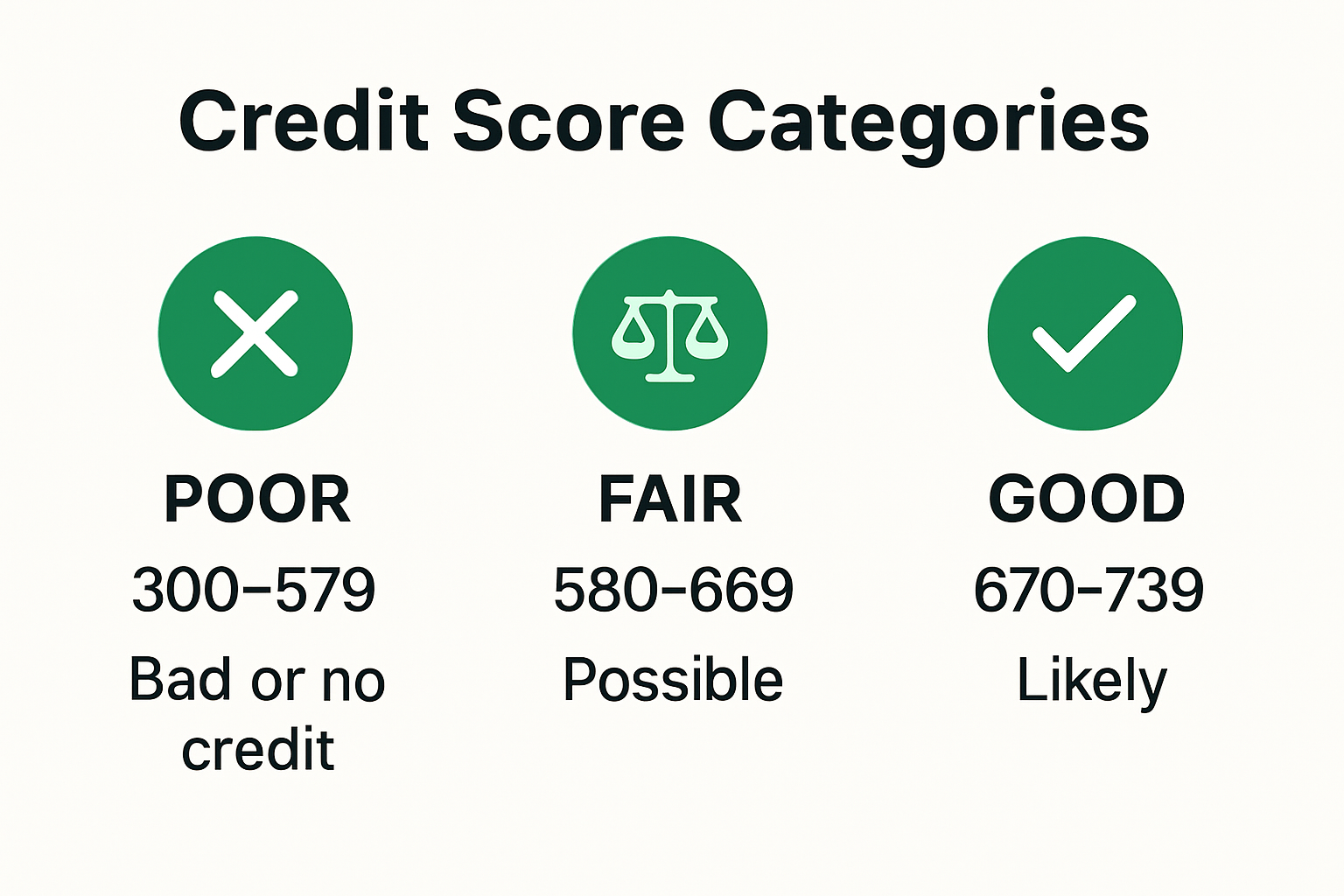

Credit scores play a critical role in loan approvals, but they are not the sole determinant. According to USA.gov, lenders assess several key elements when evaluating applications. Bad credit typically ranges between 300-579, which traditionally signals higher risk. However, modern financing approaches recognize that a low score does not automatically disqualify an applicant.

Understanding credit score categories helps set realistic expectations:

- Poor Credit (300-579): Requires more documentation and potentially higher interest rates

- Fair Credit (580-669): Indicates potential for improvement and more flexible terms

- Good Credit (670-739): Generally provides more favorable financing options

Alternative Approval Criteria

Financial institutions increasingly use comprehensive evaluation methods beyond credit scores. The U.S. Department of Education highlights that lenders often consider alternative indicators of financial reliability. These may include:

- Employment Stability: Consistent income and job history

- Debt-to-Income Ratio: Total monthly debt compared to gross monthly earnings

- Residence Verification: Proof of stable living arrangements

- Payment History: Consistent payments on existing obligations

These factors demonstrate financial responsibility and can compensate for past credit challenges. Lenders want evidence that you can manage financial commitments reliably.

Strategies for Improving Approval Chances

Proactive steps can significantly enhance your likelihood of getting approved. Gather comprehensive documentation that showcases your financial stability. This might include recent pay stubs, tax returns for self-employed individuals, and reference letters verifying income consistency.

Consider exploring alternative financing options that specialize in working with credit-challenged applicants. Some lenders focus on understanding individual circumstances rather than relying solely on traditional credit metrics.

Preparing a larger down payment can also strengthen your application. By reducing the lender’s risk, you demonstrate commitment and financial planning. Additionally, having a cosigner with stronger credit can provide additional reassurance to potential lenders.

Remember that each application and lender has unique requirements. Being transparent about your financial history, showing consistent improvement, and providing comprehensive documentation are key strategies for successfully navigating the approval process.

To provide a quick reference, the following table summarizes how different credit score ranges affect loan approval requirements and likely terms:

| Credit Score Range | Classification | Typical Requirements | Likely Loan Terms |

|---|---|---|---|

| 300-579 | Poor Credit | Extra documentation, higher down payment | Highest interest rates |

| 580-669 | Fair Credit | Standard documentation, flexible terms | Moderate interest rates |

| 670-739 | Good Credit | Basic documentation | Favorable interest rates, more offers |

Key Steps to Boost Your Approval Chances

Improving your approval chances requires strategic financial planning and proactive credit management. While bad credit can seem like an insurmountable barrier, several targeted approaches can significantly enhance your likelihood of securing auto financing.

Building and Repairing Credit Foundation

Establishing a solid credit foundation is crucial for future approvals. According to the College Foundation of North Carolina, individuals can start rebuilding credit through fundamental financial practices. Opening a checking and savings account demonstrates financial responsibility and provides a baseline for potential lenders to assess your monetary management skills.

Key strategies for credit rebuilding include:

- Consistent Bill Payments: Develop a track record of timely payments across all financial obligations

- Credit Card Management: Maintain low balances and avoid maxing out available credit limits

- Income Verification: Establish steady employment to show financial stability

The Oregon Division of Financial Regulation recommends limiting the number of credit cards and regularly monitoring credit reports to track progress and identify potential improvements.

Leveraging Alternative Credit-Building Tools

Modern financial technology offers innovative ways to build credit beyond traditional methods. Secured credit cards provide an excellent opportunity for individuals with limited or damaged credit history. These cards require a cash deposit that becomes your credit limit, minimizing risk for lenders while allowing you to demonstrate responsible credit usage.

Additional alternative credit-building tools include:

- Credit-Builder Loans: Small loans designed specifically to help establish credit history

- Authorized User Status: Being added to a responsible family member’s credit card

- Reporting Rent and Utility Payments: Some services now allow reporting of consistent non-credit payments

Preparing a Comprehensive Application

Beyond credit score improvement, creating a robust loan application increases approval likelihood. Gather comprehensive documentation that showcases your financial stability. This might include:

- Detailed employment verification

- Proof of consistent income

- Bank statements demonstrating financial management

- References that can vouch for your reliability

Consider exploring specialized financing options that work with credit-challenged applicants. These lenders often use more holistic evaluation methods, looking beyond traditional credit metrics.

A larger down payment can also dramatically improve your approval chances. By reducing the lender’s potential risk, you demonstrate financial commitment and planning. If possible, save aggressively to provide a substantial upfront payment.

Remember that credit improvement is a journey. Consistent effort, patience, and strategic financial decisions will gradually enhance your creditworthiness. Each positive action moves you closer to your goal of securing auto financing, regardless of your current credit situation.

The next table compares several alternative credit-building tools, outlining their requirements and impact on your credit profile:

| Credit-Building Tool | Basic Requirement | Impact on Credit History |

|---|---|---|

| Secured Credit Card | Cash deposit as limit | Builds revolving credit, reports monthly |

| Credit-Builder Loan | Small regular loan payments | Builds payment history on installment loans |

| Authorized User Status | Added to another’s established card | Benefits from primary user’s history |

| Reporting Rent/Utilities | Consistent on-time payments | May add non-traditional accounts to file |

Special Strategies for First-Time Buyers and Self-Employed

First-time buyers and self-employed individuals face unique challenges when seeking auto financing. These groups often encounter additional scrutiny from lenders due to perceived financial instability and limited credit histories.

Navigating Documentation Requirements

Self-employed applicants must prepare more comprehensive financial documentation compared to traditional employees. According to the Internal Revenue Service, lenders typically require detailed proof of income stability. This includes:

- Tax Returns: Minimum of two years of complete tax returns

- Profit and Loss Statements: Detailed financial records demonstrating consistent income

- Bank Statements: Showing regular cash flow and financial management

First-time buyers should similarly focus on presenting a clear financial picture. The Consumer Financial Protection Bureau recommends gathering comprehensive documentation that demonstrates financial responsibility.

Leveraging Alternative Income Verification

Traditional income verification methods often challenge self-employed individuals. Creative approaches can help overcome these obstacles:

- 1099 Income Documentation: Collect comprehensive records of independent contractor earnings

- Client Contracts: Provide evidence of ongoing business relationships

- Digital Payment Platforms: Use statements from platforms like PayPal or Stripe to verify income

First-time buyers can similarly benefit from alternative verification methods. This might include:

- Scholarship or Grant Documentation

- Part-time Work Verification

- Internship or Training Program Confirmations

Strategic Financing Approaches

Both first-time buyers and self-employed individuals can improve their approval chances through strategic planning. Credit Correct Auto recommends several targeted strategies:

- Larger Down Payments: Reduce lender risk by offering substantial upfront payments

- Cosigner Options: Consider adding a cosigner with established credit history

- Specialized Lender Selection: Target lenders experienced with non-traditional income sources

Building a strong financial profile requires patience and strategic planning. For self-employed individuals, maintaining meticulous financial records is crucial. First-time buyers should focus on demonstrating financial responsibility through consistent income and careful money management.

Understand that each lender has unique requirements. Some may specialize in working with self-employed applicants or first-time buyers. Research thoroughly, prepare comprehensive documentation, and remain persistent. Your unique financial situation does not preclude you from securing auto financing.

Remember that approval is about demonstrating reliability. Consistent income, responsible financial management, and a clear approach to debt can overcome traditional lending barriers. Whether you’re a freelancer, recent graduate, or first-time car buyer, strategic preparation is your most powerful tool in securing the financing you need.

Common Mistakes That Cause Declines

Auto financing declines can often be traced back to preventable errors that significantly impact an applicant’s approval chances. Understanding these common pitfalls is crucial for navigating the complex landscape of vehicle financing.

Credit Report Inaccuracies and Oversights

Credit report errors can derail financing applications before they even begin. According to the Federal Trade Commission, inaccurate or outdated information represents a critical obstacle for many applicants. Unpaid debts and insufficient credit history can trigger immediate application rejections.

Common credit report mistakes include:

- Incorrect Personal Information: Mismatched names, addresses, or social security numbers

- Unresolved Debt Collections: Unpaid accounts that remain unaddressed

- Duplicate Negative Entries: Multiple listings of the same negative financial event

Proactive strategies involve:

- Obtaining free annual credit reports

- Carefully reviewing all entries

- Disputing any inaccuracies immediately

- Providing documentation to support corrections

Financial Red Flags for Lenders

Lenders scrutinize multiple financial behaviors that signal potential risk. High debt-to-income ratios, frequent job changes, and inconsistent income streams can trigger automatic declines. Multiple recent credit applications also raise significant warning signs.

Key financial behaviors that compromise approval include:

- Excessive Credit Utilization: Maxing out credit cards

- Frequent Job Transitions: Showing employment instability

- Multiple Hard Credit Inquiries: Applying for multiple credit lines simultaneously

- Incomplete or Inconsistent Application Information

Strategic Application Preparation

Avoiding common mistakes requires comprehensive preparation. Credit Correct Auto recommends developing a strategic approach to financing applications:

- Consolidate and pay down existing debts

- Stabilize employment before applying

- Create a comprehensive financial documentation package

- Understand and address potential negative credit factors

Preparing a robust financial narrative involves demonstrating consistent income, responsible debt management, and clear financial goals. Lenders want evidence of reliability beyond simple credit scores.

Understand that each declined application can further damage your credit profile. Strategic preparation means anticipating potential issues before submitting an application. This might involve working with a financial advisor, credit counselor, or specialized auto financing consultant who can provide personalized guidance.

Remember that a decline is not a permanent roadblock. Each rejection provides an opportunity to reassess your financial strategy, address underlying issues, and develop a more compelling application for future submissions. Patience, preparation, and persistent financial improvement are your most powerful tools in overcoming financing challenges.

Frequently Asked Questions

How can I get approved for a loan with bad credit in 2025?

To improve your chances of loan approval with bad credit in 2025, focus on building a strong financial profile by demonstrating consistent income, providing comprehensive documentation, and considering larger down payments.

What credit score is considered bad in the U.S.?

In the U.S., a credit score below 580 is typically considered bad. This range indicates a higher risk for lenders, potentially leading to more stringent loan terms.

Are there alternative ways to get a loan if I have no credit?

Yes, some lenders offer alternative financing options that assess your financial reliability beyond traditional credit scores. This may include evaluating your income stability, employment history, and other financial indicators.

What common mistakes should I avoid when applying for a loan?

Common mistakes include inaccuracies in your credit report, having high debt-to-income ratios, and providing inconsistent information in your loan application. Ensure to review your credit report and stabilize your finances before applying.

Ready to Get Approved for Auto Financing in 2025?

If you are struggling with bad credit, no credit, or even past declines, you know how discouraging the approval process can feel. The article you just read shows that lenders now look beyond just your credit score. But you still need the right partner to turn your preparation into real results. At Credit Correct Auto, we understand the fear of rejection and the frustration of endless paperwork. Our expert team offers a fast, judgment-free solution for people dealing with credit challenges. We connect you with understanding lenders who consider your full financial story, not just a number. Most customers receive an answer in under a minute.

Take control of your car ownership journey and stop letting your credit history hold you back. Visit our How It Works page to see how simple and straightforward the process can be. Or go right to Credit Correct Auto and start your application now. Drive toward approval and rebuild your confidence today. Your future starts with one easy step.